Mortgage Rates Today: What's Really Going On With 30-Year & Refinance Rates?

Mortgage Rates Are Up (Again). Is the Fed Just Messing With Us?

Look, if you’re anything like me, you probably woke up this morning, checked your phone, and saw the headlines screaming about mortgage rates ticking up. Again. And then, because the universe loves a good joke, you scrolled a little further and found some "expert" from the New York Fed talking about how rate cuts are still on the table for December. Give me a break. Are they serious? Or are we just stuck in some kind of financial Groundhog Day where the same vague promises keep recycling while our wallets get lighter?

The Fed's Favorite Game: "Will They, Won't They?"

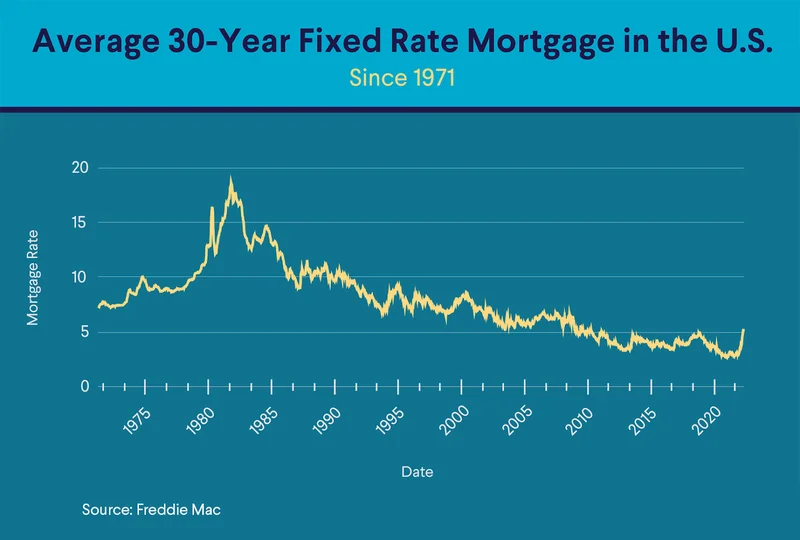

So, the Bankrate data drops, telling us what anyone trying to buy a house or refinance already knows: 30-year fixed, 5/1 ARMs, jumbo loans—they all edged higher. 30-year mortgage rates increase - Should you wait? | Today's mortgage and refinance rates, November 24, 2025. No surprise there, right? But then, like a magician pulling a rabbit out of a hat that’s clearly rigged, New York Fed President John Williams pipes up. He’s out there in Santiago, Chile, of all places, casually mentioning that "downside risks to employment have increased" and "upside risks to inflation have lessened somewhat." Oh, really?

My guy, Williams, says rate cuts are still on the table. Still. It’s like they’re dangling a piece of prime steak in front of a hungry dog, just to watch us salivate. He claims the labor market's cooling, but inflation risks are down. Okay, I get it. They're trying to walk a tightrope, balancing a cooling job market against "sparking higher inflation." But honestly, after years of watching these guys, it feels less like a tightrope walk and more like they're just throwing darts at a board blindfolded, hoping something sticks. And then they call it "monetary policy." This ain't policy; it's a guessing game, and we're the ones paying the entry fee.

What I wanna know is, who are these "upside risks to inflation" lessening for? Because it sure ain’t for me when I’m at the grocery store.

The Disappearing Act and the Expert Spin

Here’s where it gets good. Right after Williams’ speech, the yield on the 10-year Treasury bond — you know, the thing our fixed mortgage rates are supposedly tied to — slid to its lowest rates this month. So, on one hand, mortgage rates are up. On the other, the thing they’re tied to is down. How does that even compute? It's like trying to explain to my five-year-old why his ice cream cone melted before he could eat it, but also, it's still frozen. It defies logic.

And then we get the "expert" commentary. Mark Hamrick, a senior economic analyst for Bankrate, chimes in with this gem: “Americans are every bit as challenged on the outlook for the economy as are Federal Reserve officials.” No kidding, Sherlock. You mean the people whose lives are actually impacted by these decisions are as confused as the folks making them? What an insight! He adds, "Employment prospects are tied to both hopes and the reality of wage gains, which provide a path to managing elevated prices." Right. Because "hopes" are a solid financial strategy. My hopes ain't gonna pay my mortgage, Mark.

What exactly are these officials doing if they're as "challenged" as the rest of us? Are they just sitting around in fancy conference rooms, sipping artisanal coffee, and shrugging? I picture them, suits pressed, staring blankly at charts, a single bead of sweat trickling down someone's brow as they ponder whether to cut rates by 0.25% or 0.50%. The stakes are so low for them, but for us, it's the difference between affording a home or being priced out forever.

The December Mirage and Our Collective Anxiety

So, the Fed’s next meeting is December 9th and 10th. And if "the weeks leading up to the Fed's rate cuts in September and October are any indication," mortgage rates could continue to trend downward. Could. That's the key word, isn't it? It’s always "could." It’s a classic bait-and-switch. They get us all hyped up, talking about potential cuts, and then, boom, rates stay high, or even creep up further. It's like Lucy pulling the football away from Charlie Brown, every single time. And offcourse, we fall for it.

Hamrick tries to temper expectations: “Ultimately, whether we see a December rate cut or not won't make or break households.” Oh, really? Tell that to the millions of people who are trying to figure out if they can afford that home mortgage rate today, or if they need to hold off on their dreams. Tell that to the folks hoping for better refinance rates today to free up some cash. A small change in the current mortgage rates can absolutely "make or break" a household budget. This isn't just about "financial markets balancing their understanding of the present." This is about actual people, with actual lives, trying to navigate an economy that feels increasingly rigged against them.

Maybe I'm the crazy one here for expecting a straight answer, for wanting clarity instead of this constant, agonizing uncertainty. But ain't that the whole point of these institutions? To provide some kind of stability?

They're Just Kicking the Can

Here's the brutal truth: the Fed, like a bad sitcom writer, is just dragging out the plot. They know everyone's watching the 30 year mortgage rates, hoping for a break. They know what are mortgage rates today is the question on everyone's mind. But instead of decisive action, we get speeches in Chile and internal squabbles. It’s not about "balancing" risks; it’s about avoiding responsibility for as long as possible. They're playing a long game, and we, the actual homeowners and hopeful buyers, are just pawns in their endless, bureaucratic chess match. Don't hold your breath for December. You'll pass out before they give us a real win.

Related Articles

Rigetti Computing (RGTI) Secures $5.7M Quantum Order: Dissecting the Bull Case After its 9.6% Jump

Decoding Rigetti's Quantum Leap: Is a $5.7M Sale Worth a 25% Stock Pop? The news, when it hit the wi...

Fifth Third Swallows Comerica for $10.9B: Why It's Happening and Why You Should Care

So, another Monday, another multi-billion dollar deal that promises to "create value" and "drive syn...

Dan Schulman Named New Verizon CEO: What His PayPal Past Means for Verizon's Future

Verizon’s New CEO Isn’t About 5G. It’s About a Quiet Panic. The market’s reaction to the news was, i...

Uber Stock: Price, Earnings, and Outlook

Uber's Q3 Looks Good, But Its Future Value Is Still Driving Through a Fog of Autonomous Uncertainty...

RGTI Stock: A Comparative Analysis vs. IONQ and NVDA

The market action surrounding Rigetti Computing (RGTI) in 2025 presents a fascinating case study in...

The $5.2 Billion Bet on Akero Therapeutics: What This Means for the Future of Medicine

Here is the feature article for your online publication, written in the persona of Dr. Aris Thorne....